Overcoming Data Integration Challenges in Financial Institutions

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Overcoming Data Integration Challenges in Financial Institutions

%20(1).png)

N Suresh

Join us on November 6th as Mr. Yash Mishra, Product Manager, Fatakpay, reveals the precise strategies that eliminates the speed trap and guarantees a 30% conversion boost.

Data is money. Data is control. Data is trust.

And, data integration in banking and financial services is a business-critical mandate. Beyond connecting systems for transaction processing, it engineers a unified, intelligent, and secure data ecosystem that delivers a 360-degree, real-time view of operations, customer behavior, regulatory compliance, and risk exposure.

When data flows seamlessly across core banking platforms, customer relationship management (CRM) tools, loan origination systems, and customer service channels, financial institutions gain more visibility and velocity. They act faster, personalize deeper, and compete smarter.

In this blog, we unpack how financial institutions can overcome data integration challenges, fortify data security, and set the foundation for agile, insight-driven operations.

The Importance of Data Integration in Banking and Financial Services

The modern financial institution juggles thousands, sometimes millions of data points daily, across multiple channels:

- Mobile banking apps

- Payment gateways

- CRM systems

- Wealth management platforms

- Regulatory compliance databases

- Risk management systems

When these data points exist in isolation, they create bottlenecks, redundant processes, and compliance risks. Today, a financial institution is only as agile as its integrated data systems.

Think of a common customer journey today: one person might interact with a bank through a mobile app, website chatbot, in-person visit, and a call center, all in a week. If these channels aren’t speaking the same data language, that customer is effectively a different person in each interaction. It’s inefficient and damaging to your brand, trust, and customer service.

This is where data integration becomes mission-critical.

Siloed data has a direct negative impact on financial operations. These silos delay decision making and create blind spots in compliance, risk assessment, customer experience, and revenue and sales forecasting.

Integrated data unlocks a unified view of the customer, and that’s the foundation for personalized banking, predictive analytics, real-time risk mitigation, and agile product innovation.

From streamlining internal workflows to transforming the onboarding experience, the importance of data integration in banking and financial services cannot be overstated. In an industry where milliseconds matter - in loan approvals, fraud detection, investment decisions, data must flow without friction.

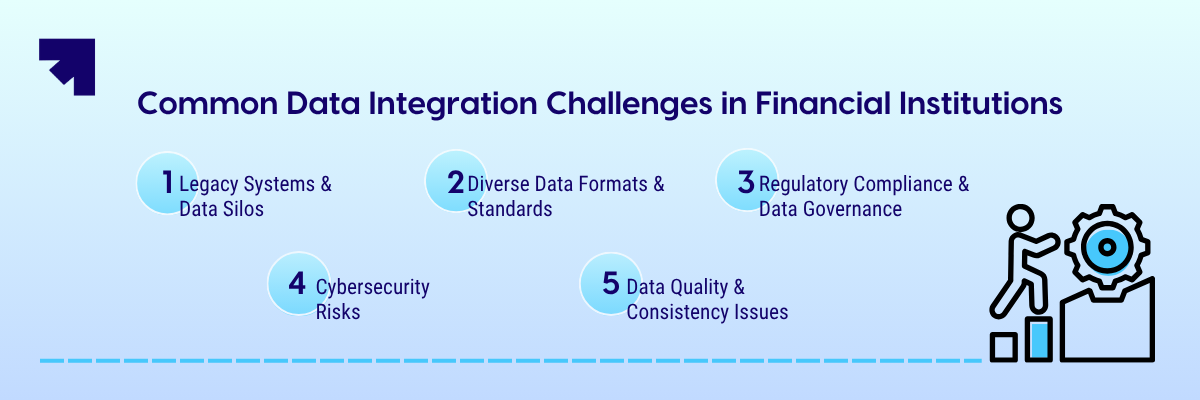

Common Data Integration Challenges in Financial Institutions

While the benefits of integration are undeniable, achieving it is far from straightforward. Financial institutions often find themselves tangled in a web of legacy systems, conflicting standards, and rising compliance expectations, all while the threat of cyberattacks looms large.

Here’s a deeper look at the most pressing integration challenges in the banking and financial services landscape:

1. Legacy Systems and Data Silos

Despite rapid advancements in fintech, many banks are still anchored to core banking systems built 20-30 years ago. These systems were designed for batch processing, not for real-time, customer-centric digital ecosystems. 55% of banking executives say legacy infrastructure is the biggest hurdle to transformation.

And it's not just the age of the technology, it's the fragmentation it causes. Marketing, compliance, credit risk, and customer service all maintain their own datasets, resulting in disconnected customer insights, duplicate efforts, and missed opportunities.

Without breaking down silos, banks can't deliver personalized services, detect fraud patterns early, or comply with regulatory reporting, putting them at serious competitive disadvantage.

2. Diverse Data Formats and Standards

Financial institutions manage massive volumes of structured and unstructured data - from transactional records, mobile apps, scanned documents, credit bureaus, core banking systems, call centers, you name it.

The problem?

Each source speaks a different language, different structures, formats, metadata, and standards across incompatible systems, making integration a nightmare.

Beyond technical incompatibility, departmental fragmentation adds fuel to the fire: with risk, marketing, operations, and compliance all speaking different “data languages.” This disjointedness hinders real-time decision-making, blocks automation initiatives, and weakens efforts to deliver personalized client experiences.

3. Regulatory Compliance and Data Governance

In the financial sector, compliance is non-negotiable. Each financial institution must comply with an alphabet soup of regulations :

- Payment Card Industry Data Security Standard (PCI DSS)

- Federal Financial Institutions Examination Council (FFIEC)

- Dodd-Frank Act

- Basel III guidelines

And each has its own stringent rules on how data is collected, processed, stored, and shared. Every integration point, every movement of data, must be tracked, logged, and secured. Failure to align integration efforts with these regulations can result in millions in fines, reputational harm, and even operational shutdowns.

Yet, achieving compliance isn't just about ticking boxes. It requires strong data governance frameworks with clear policies around data access, consent, lineage, and retention.

4. Cybersecurity Risks

More connections mean more vulnerabilities. It’s that simple. Every API call, every third-party SaaS connection, every cross-system data transfer introduces a new potential vulnerability.

Poorly integrated environments often lack consistent security controls, making them attractive targets for cybercriminals.

Deloitte warns that without robust, multi-layered cybersecurity embedded into the integration process, financial institutions are vulnerable to catastrophic breaches, not just of customer data, but also of trust.

Major Integration Risks Include:

- API security failures

- Inconsistent identity management

- Data exposure during migration

- Insider threats across hybrid systems

5. Data Quality and Consistency Issues

Here’s a harsh truth: No amount of integration can fix bad data. It will only amplify the problem. Before integrating, financial institutions must clean, validate, and enrich their datasets; otherwise, they risk automating chaos.

Gartner estimates that poor data quality costs organizations an average of $12.9 million per year in losses. Many institutions attempt to integrate datasets that are:

- Duplicated

- Incomplete

- Outdated

- Conflicting

Without accurate data, banks risk failed digital initiatives, alienated customers, failed regulatory audits, and strategic missteps.

Strategies for Streamlining Financial Data Systems

Far from only a systems issue, data fragmentation carries substantial business consequences. For financial institutions, real-time, accurate data flow across customer touchpoints, risk systems, compliance platforms, and operational backends is non-negotiable. True data integration demands a foundational shift, aligning IT architecture, security posture, and business strategy.

Here’s how leading banks and financial services organizations are addressing this integration imperative:

1. Implementing Advanced CRM Architectures

Traditional CRMs often operate in silos, disconnected from the enterprise data warehouse (EDW), loan origination systems, KYC/AML platforms, and regulatory reporting layers. Advanced financial services CRMs are now built on open APIs, cloud-native containers, and real-time data pipelines, enabling horizontal integration across platforms.

High-performing CRM ecosystems enable:

- 360° customer visibility: Integrating KYC data, interaction history, transactional insights, and product holdings in one interface.

- Cross-functional synchronization: Connecting marketing, lending, support, and advisory teams.

- Data-driven recommendations: Powering predictive financial guidance through AI.

2. Leveraging AI and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) algorithms can automate data integration processes, identify patterns, and predict customer behavior. These technologies enable CRM analytics personalization, allowing financial institutions to offer tailored products and services.

- ML-based data matching and deduplication (using probabilistic record linkage algorithms) improve customer master records during data integration.

- NLP (Natural Language Processing) engines can extract structured data from unstructured sources (emails, contracts, voice transcripts) for integration into CRMs and risk engines.

- Behavioral analytics models trained on integrated transactional and demographic data enable real-time personalization.

AI doesn’t just clean data, it learns from it. For instance, AI can detect early signs of financial distress (e.g., declining deposits + delayed EMI payments), triggering proactive interventions like financial coaching or restructuring offers.

3. Client Onboarding as a Data Integration Touchpoint

Client onboarding in financial services is the most intensive moment. It is heavily dependent on third-party systems, credit bureaus, ID verification APIs, AML screening engines, and eKYC platforms. If data integration is fragmented at this stage, downstream client servicing suffers. But data integration must start from day one. Automating client onboarding in financial services using CRM-integrated workflows accelerates verification while maintaining compliance.

Modern onboarding platforms enable:

- E-KYC integration with credit bureaus and verification APIs

- Seamless document capture, categorization, and storage

- Real-time profile creation in the CRM and core systems

Mitigating Cybersecurity Risks in Financial Institutions

As data integration efforts increase system interdependencies, they also expand the attack surface. Poorly secured APIs, unmonitored data lakes, or misconfigured Identity and Access Management (IAM) policies are common breach vectors. The World Economic Forum ranks cyber risk among the top 5 threats to global financial stability.

In an integrated environment, a single vulnerability can expose terabytes of sensitive data, leading to fines, reputational damage, and customer churn. To safeguard integrated systems, institutions are applying zero trust principles, embedding security by design, and implementing end-to-end visibility frameworks.

1. Regular Security Audits and Compliance Checks

Security isn’t a once-a-year audit. It’s a living, breathing process. Institutions must implement:

- Penetration testing across all integrated systems

- Automated compliance monitoring (e.g., General Data Protection Regulation (GDPR), Federal Financial Institutions Examination Council (FFIEC), Reserve Bank of India (RBI), Payment Card Industry Data Security Standard (PCI DSS))

- Data classification protocols to determine sensitivity and access levels.

2. Employee Cyber Hygiene & Awareness

Human error is a significant factor in data breaches. Despite sophisticated tools, major breaches in financial services originate from human error. Educating employees about cybersecurity best practices reduces the risk of accidental data leaks. Institutions should also invest in inbound email security solutions to detect phishing attempts, malicious attachments, spoofed domains, and other email-based threats before they reach employees. Also, institutions must:

- Embed cybersecurity into onboarding and regular training

- Simulate phishing attacks and response drills

- Use role-based access controls to limit exposure

Foster a security culture to minimize human error in banking institutions.

3. Implementing Advanced Security Architecture

It’s not enough to rely on basic firewalls and anti-virus software. Integration demands deep endpoint and system-level protection.

Critical security tools to implement:

- Zero Trust Architecture (ZTA): Never trust, always verify, even inside your network

- Multi-Factor Authentication (MFA): Reduces credential-related breaches by 99.9%

- Behavioral Anomaly Detection: AI-based tools that spot suspicious data access in real time

- Data Encryption at Rest and in Transit: Ensures sensitive data is protected when stored and during transmission, preventing unauthorized access and interception

Build a System That Works as One

The future of financial services belongs to institutions that think holistically, where systems speak the same language and defenses are as dynamic as the threats they face. Whether you're a credit union, private bank, or fintech, the question is no longer if you’ll integrate and secure, it's how fast and how well.

If you're ready to modernize with intelligence, security, and scale, Corefactors CRM and RevOps platform is designed to be your command center.

- Unified customer intelligence

- Seamless system integrations

- Enterprise-grade security

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Frequently Asked Questions (FAQs)

Why is data integration important in banking and financial services?

Data integration enables financial institutions to have a unified view of customer information, streamline operations, and make informed decisions, leading to improved customer satisfaction and compliance.

How does CRM analytics personalization benefit financial institutions?

CRM analytics personalization allows institutions to tailor their services based on customer behavior and preferences, enhancing engagement and loyalty.

What are effective data breach prevention strategies?

Effective strategies include regular security audits, employee training, implementing advanced security solutions, and ensuring compliance with regulatory standards.

How can Corefactors assist in data integration?

Corefactors provides a robust CRM platform that facilitates seamless data integration, enhances customer experiences, and ensures regulatory compliance, helping financial institutions overcome integration challenges.

.png)

.png)